June 05, 2026 | 7 Minute Read

Key Takeaway

We believe investors should consider allocating to EM debt for diversification given that EM economies currently have limited exposure to the AI investment cycle and could prove to be more resilient to potential AI labor shocks compared to the US.

In the US, It’s AI and Then Everything Else

Depending on where you look, AI is a paradigm-shifting productivity windfall, the driver of a massive equity bubble or a societal wrecking ball set to displace huge swathes of the American labor force. Which one will it be? In much the same way that widespread adoption of the internet gave us both the dot-com bubble and a paradigm-shifting economic reorientation, we know now that things will likely change because of AI but not exactly how they’ll change.

AI-related valuation expansion is driving the stock market ever higher, triggering greater interest by tech companies in investing in AI, even where the marginal return on capital appears uncertain. That rally is creating a wealth effect which is helping propel the “K-shaped” economy. It’s also driving a capex cycle that is doing almost all of the heavy lifting in terms of US economic activity. The funding cycle allowing both of these dynamics to persist is being propelled by tight credit spreads and inflows of equity capital from abroad (principally from the Middle East and Asia)

Reconciling AI Fundamentals, Valuations and Technicals

Amidst this ebullient atmosphere, valuations feel a bit disconnected from any storyline not involving a massive productivity windfall that simultaneously doesn’t separate an increasingly AI-skeptical labor force from its paychecks. We hope that will be the case. But if it’s not, a key question for portfolio managers and asset allocators is how to construct portfolios that will be resilient against AI-related volatility.

Higher-quality fixed income typically provides an effective hedge against economic or market downturns. With US credit spreads of 72 bps near all-time tights however, we believe it makes sense to explore how other asset classes, such as emerging markets (EM) debt, can improve both portfolio returns and diversification.1

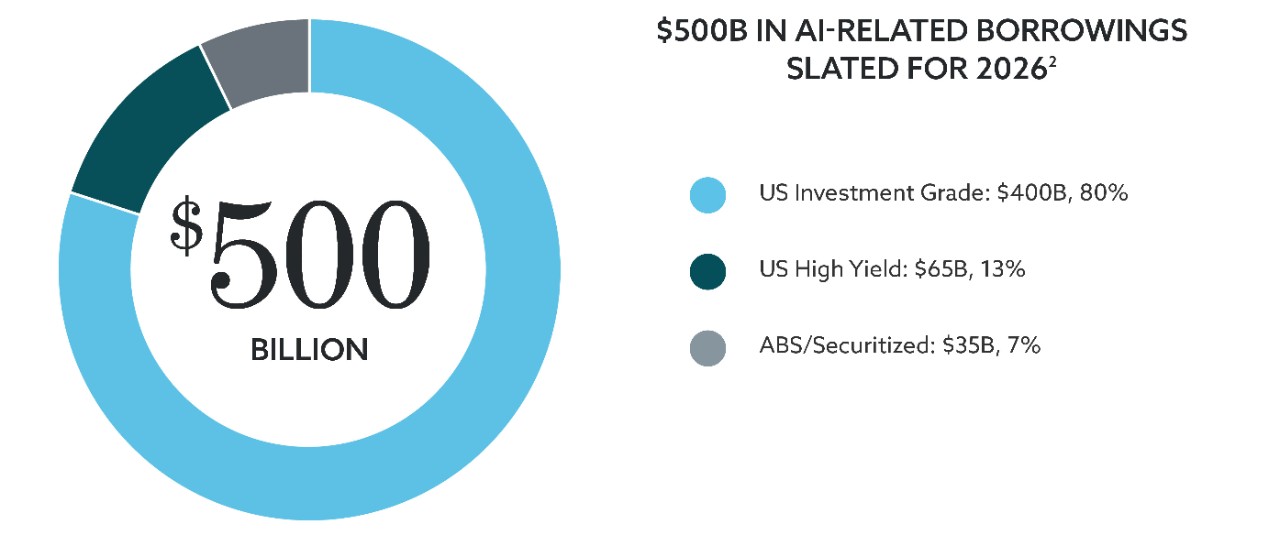

It’s not just that spreads are tight. US credit markets have also become an important enabler for the AI growth story with $500B estimated to be borrowed to fund AI investments in 2026.2 While $500B isn’t a huge quantum in the context of an $8T US investment grade (IG) corporate credit universe, the Technology sector’s increasing index weight is reminiscent to us of previous heavy issuance cycles in Telecom and Energy that ended in tears.3

EM Debt Can Offer Insulation from AI Volatility

While investors often think of EM equities as a key building block of international diversification, common stock indices such as the MSCI EM index are currently highly concentrated in Asian technology companies. Such indices have a high correlation to US AI stock moves, while also being vulnerable to strength in the US dollar (USD). Instead, we find that USD-denominated EM debt can enjoy more diversification benefits versus US stocks, while avoiding some of the pitfalls of current US credit markets.

We see EM debt as being well-positioned against both fundamental and valuation risks stemming from AI dominance. For good or ill, EM economies outside of several advanced east Asian countries have limited exposure to the AI investment cycle, whether in chips, data centers or the related infrastructure investment. What we see many EM economies do is “sell shovels to the gold rush”, so to speak, in terms of critical minerals and raw materials to facilitate the global buildout of new energy infrastructure. Regardless of whether AI animal spirits or actual investments roll over, we believe EM economic growth should continue to benefit from insatiable global energy demand, especially given structural commodity supply constraints that were in place before the current rally.

Given their less-developed starting points, EM economies would also appear to be more resilient to future AI labor shocks. Only 12% of workers in low and low-middle income countries are classified as white collar versus a much more concerning 44% of the labor force in the US.4 As we’ve seen in the case of other technological jumps such as mobile phones and digital payments, EM countries’ earlier stage of development could make them more adaptable to AI-related labor disruption.

Digging into the impact of AI investment on credit markets, an explosion of data center financings in US credit markets has created a significant gap between US and EM vulnerability to an AI slowdown. One common EM bond index has only about 1% exposure to technology companies versus over 12% (and rapidly growing) for the US corporate universe.5,6 EM debt also tends to have less leverage in the system, with IG-rated EM companies having about 60% less leverage on their balance sheets than US IG issuers on average.7 In an AI investment crunch, we believe that EM spreads could compress versus US peers.

Whether the current AI market frenzy ends in a crash or just a reversion to the mean, we think now is the time to start planning ahead to prepare your portfolios. In our view, EM debt has been a meaningful addition to fixed income allocations in recent years, and we believe that its combination of moving up the development curve AND AI resilience should justify a second look.

(1) Bloomberg. Spread of Bloomberg US Corporate Index. May 29, 2026. (2) Morgan Stanley. “Data Center Financing: Faster, Broader, Deeper.” May 26, 2026. (3) Bloomberg. Amount outstanding of Bloomberg US Corporate Index. May 29, 2026. (4) PPM estimates based on World Bank and International Labour Organization data. May 29, 2026. (5) Bloomberg. Bloomberg EM USD Aggregate Index. May 29, 2026. (6) Bloomberg. Bloomberg US Corporate Index, calculated as Technology sector plus AMZN/META. May 29, 2026. (7) J.P. Morgan. “Emerging Markets Corporate Strategy.” March 2026.

Unless otherwise stated, the information presented has been prepared from market observations and other sources believed in good faith to be reliable. Information and opinions expressed by PPM are current as of the date indicated and are subject to change without notice. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed.

Past performance is no guarantee of future results. Investments involve varying degrees of risk and may lose value.

© 2026 PPM America, Inc. All rights reserved.