June 11, 2026 | 4 Minute Read

Key Takeaway

A recent industry conference reinforced overall consumer strength amid rising food and gas prices, but select sectors like packaged goods are more challenged.

PPM analysts attended a Barclays investment grade consumer and retail conference during the last week of May. We met with several management teams across sectors and attended presentations by industry experts (e.g., Barclay's head of consumer and retail investment banking).

Going into the conference, we viewed consumer trends as bifurcated, with packaged food under considerable pressure due to headwinds including GLP-1s and affordability issues, while other parts of food (notably protein) continued to enjoy strong demand. We left the conference even more confident in our view of the US consumer.

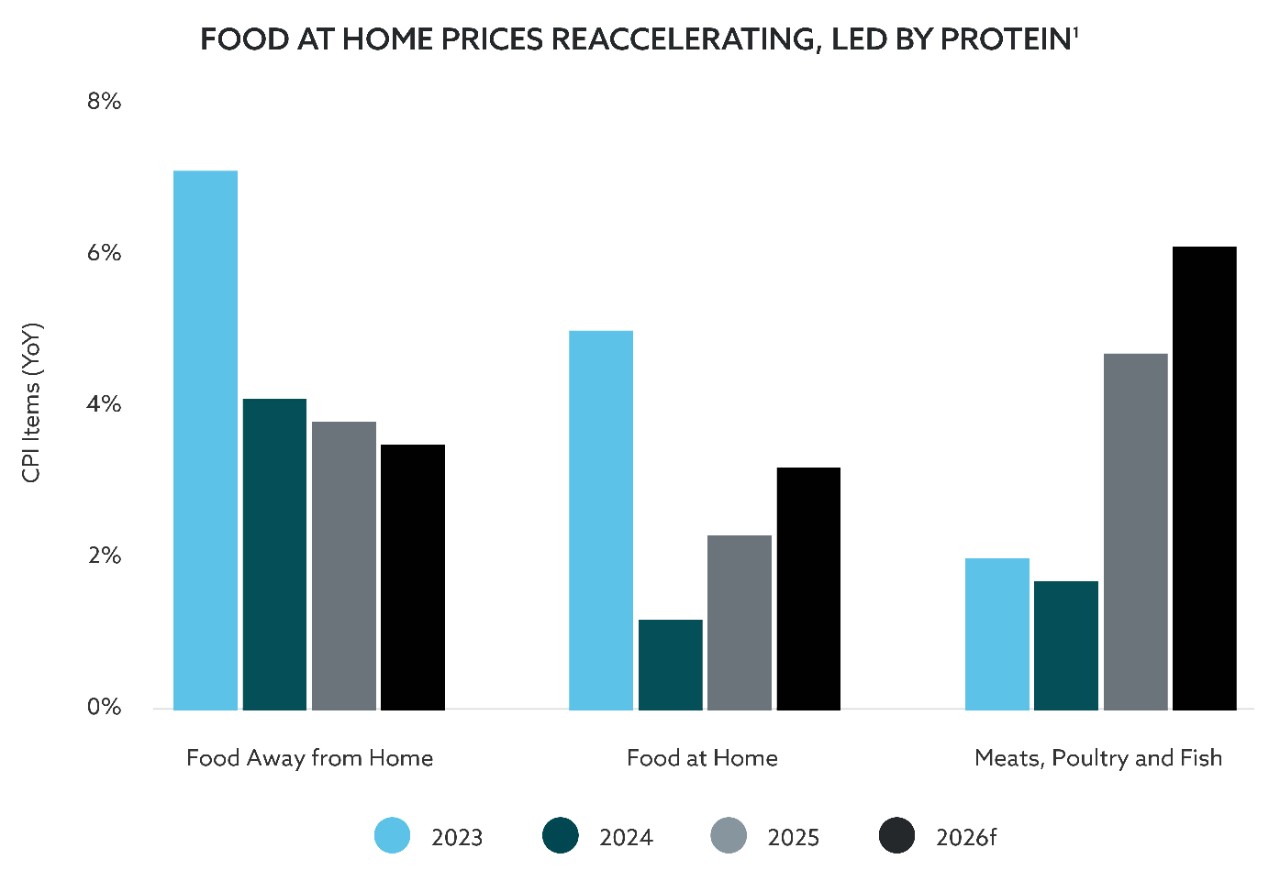

Underpinning current themes has been the run-up in food prices over the last few years. Both food away from home (7.1%) and food at home (5.0%) saw significant prices increases in 2023.1 For food away from home, price increases have decelerated toward their long-term average. For food at home, however, price increases have reaccelerated.

More recently, higher gas prices have become an increasing concern on the assumption consumers will have to offset this cost by reducing purchases elsewhere. During the conference, a large convenience store operator noted consumers are spending a fixed amount on gas (same total price, fewer gallons), but that has led to more frequent visits. A large beer company shared it has not seen a negative impact from gas prices, at least not yet (and, separately, is excited about a potential bump from the upcoming World Cup).

Packaged food could be the most challenged sector, given headwinds such as GLP-1s, SNAP cuts, private labels taking share and the focus on health/wellness. These headwinds do not appear to be abating.

Conversely, protein is one bright spot within the food sector, with strong demand driving higher prices. Meat, poultry and fish were up 4.7% in 2025 and prices are expected to rise 6.1% in 2026.1 Management teams we spoke to have not seen consumers pull back, with new health habits continuing to drive seemingly insatiable appetites for protein.

We left with two takeaways for bond markets. The first is many management teams feel their investment grade ratings are important. Amid the potential for downgrades, select names could cut dividends to prop up cash flows. The second is scale matters again, and we believe there is the potential for larger, strategic M&A.

As consumer health impacts the broader economy beyond the consumer and retail sector, our insights are also helping to drive investment rationale and positioning across the firm.

(1) US Department of Agriculture Food Price Outlook. 22 May 2026. Forecasts shown are the midpoints of the 2026 prediction intervals.

Unless otherwise stated, the information presented has been prepared from market observations and other sources believed in good faith to be reliable. Information and opinions expressed by PPM are current as of the date indicated and are subject to change without notice. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed.

Past performance is no guarantee of future results. Investments involve varying degrees of risk and may lose value.

© 2026 PPM America, Inc. All rights reserved.