June 25, 2026 | 5 Minute Read

Key Takeaway

While tighter spreads in frontier markets imply less margin for error, we believe investors should still consider the asset class given its idiosyncratic nature and relatively wide spread dispersion compared to investment grade and other ‘core’ EM markets.

Improving Story in Frontier Markets

Markets around the globe have endured multiple shocks over the past five years. In 2022 alone, the combination of Russia’s invasion of Ukraine, Fed interest rate hikes, and China’s property crisis looked like it might overwhelm frontier markets.1 Market pricing reflected worst-case scenarios: widespread defaults and poor recoveries. With a handful of exceptions, those fears were shown to be misplaced. Economic orthodoxy, prudent debt management and “bridge” financing in the form of multilateral support all helped frontier economies navigate a relentlessly challenging external environment.

That track record has not been lost on markets, with frontier debt outperforming other major credit markets in subsequent years, including through the 2025 trade war and this year’s war in Iran.2 These are the kind of shocks that, in the past, might have broken frontier. Instead, hard-currency frontier returns have outpaced both the broad EM sovereign index and its investment grade core.

The result has been an increasing number of frontier economies using market access to term out shorter-term debt and improve amortization profiles. Improving credit stories have extended the rally. And tighter spreads have paved the way for several first-time issuers to approach the market, including the Democratic Republic of Congo and Laos.

And yet, tighter spreads ultimately imply higher risks, given a more limited margin for error. This is an issue we see across fixed income assets, and frontier is no exception.

It forces us to ask the question, is there still a case for exposure to frontier markets? We contend there is, for two reasons.

First, we believe the secular frontier story remains compelling. As outlined previously, frontier still has significant potential for income convergence, in our view, given its relatively lower starting point. That implies room for potential capital appreciation over time, even from tighter starting spread levels.

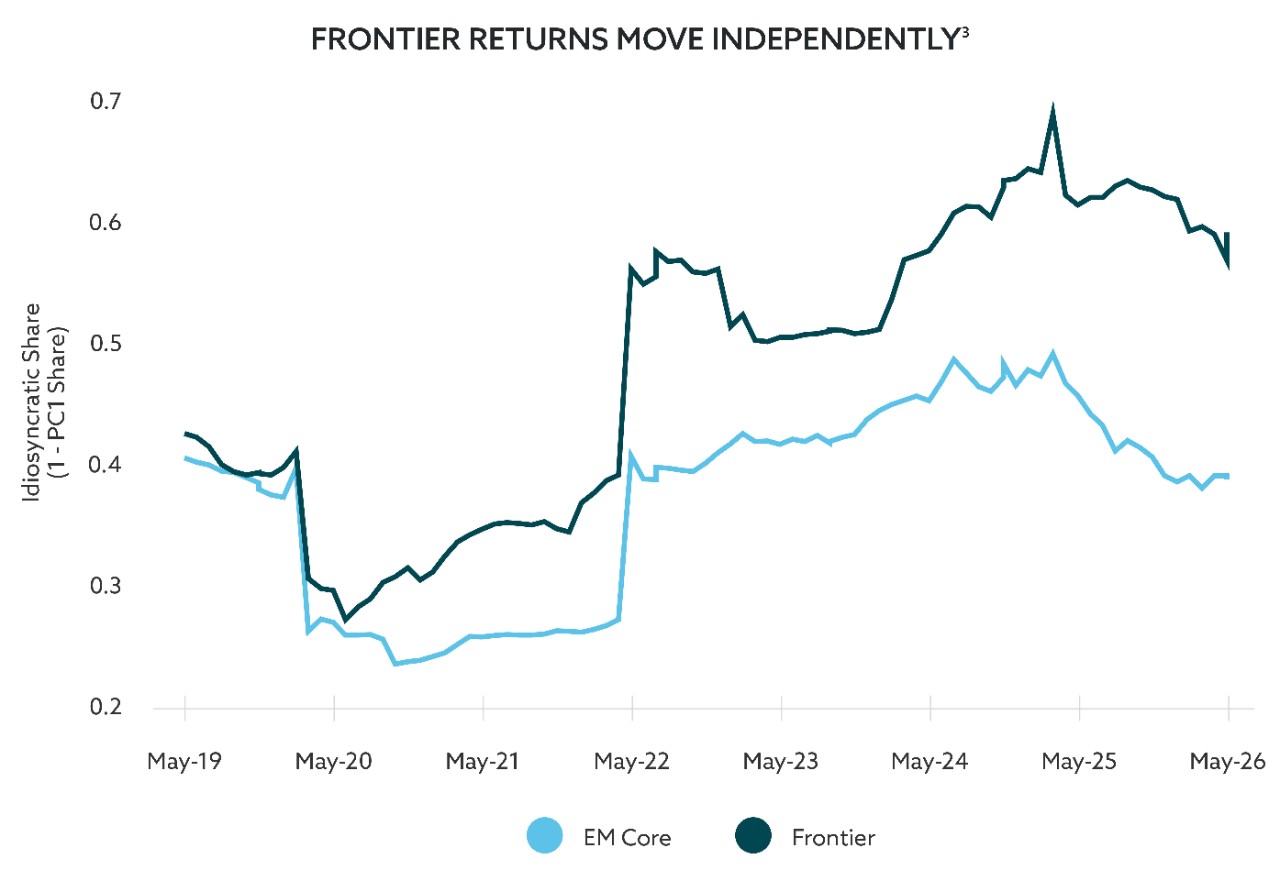

Second, and perhaps most importantly, we believe greater dispersion and a more idiosyncratic issuer mix within frontier may imply a genuine potential for credit selection to power performance, even in the context of tighter headline spread levels. Within the investment grade and ‘BB’ “core” of the J.P. Morgan EMBI Global Diversified Index, dispersion has collapsed: spreads are tight and tightly clustered. Within frontier, dispersion remains wide, and the constituents move with far less common cause. It’s much more idiosyncratic.3 We believe there are improving stories that remain attractively priced and less exposed to the global macro environment—such as Argentina—that give us the ability to focus portfolio exposures in a way that can improve risk-adjusted returns.

Risks to Consider

Getting security selection right looks increasingly important to us in the context of budding risks, where we see three risks stand out most clearly.

- Commodities now cut both ways. The Iran risk premium has started to unwind and, while the oil retreat relieves pressure on importers, it simultaneously applies fiscal and external pressure on the segment’s exporters. Neither group is in a happy (or predictable) equilibrium in our view.

- A rare and likely very strong El Niño – forecasters put the odds at roughly 60–70% – stands to disrupt agricultural output and inflation across frontier (and broader EM) economies.4 The effects are expected to be concentrated in the coming winter and compound downstream impacts from fertilizer disruptions caused by the Iran war.

- Re-assertion of US growth leadership on the back of the AI capex cycle – on track to exceed $500B this year – may reignite a shorter “US exceptionalism” cycle that pulls capital into US assets and fuels incremental dollar strength (SpaceX, Anthropic and OpenAI IPOs all represent potential “pull” factors that can support the dollar). We believe US monetary policy will be key to watch in this context (and leaves us biased to express the frontier view primarily via hard currency assets).

None of these risks change the core message. Frontier markets have earned their place in a multi-sector credit allocation, in our opinion. We believe the diversification and risk-adjusted return potential they offer remain compelling relative to alternatives. But key drivers of the early-stage recovery in returns – led by spread recompression and distressed credits curing – seem to have largely moved into the rearview mirror. We believe what lies ahead likely rewards the bottom-up, credit-intensive work of identifying credits where price still lags fundamentals (and also those where it’s run ahead of them). We like owning the asset class, but we’ve become increasingly selective in the way we do so.

(1) PPM defines frontier markets as countries at a lower level of economic development, which typically carry a below-investment grade credit rating or are classified by the World Bank as low- or lower-middle income. (2) Bloomberg. Frontier (J.P Morgan NexGem Index) cumulative total returns are 41.01% since 31 Dec 2021, compared to 14.98% for J.P Morgan EMBIG Diversified Index, 9.28% for J.P Morgan CEMBI Broad Index, 17.69% for J.P Morgan GBI-EM Global Diversified Index, 0.22% for the Bloomberg US Aggregate Index, 1.63% for the Bloomberg US Credit Index, and 20.55% for the Bloomberg US High Yield Index. 22 June 2026. (3) Bloomberg, J.P. Morgan Index Research and PPM America. 12 June 2026. (4) National Oceanic and Atmospheric Administration. “El nino forms, expected to strengthen, say NOAA forecasters.” 11 June 2026.

Unless otherwise stated, the information presented has been prepared from market observations and other sources believed in good faith to be reliable. Information and opinions expressed by PPM are current as of the date indicated and are subject to change without notice. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed.

Past performance is no guarantee of future results. Investments involve varying degrees of risk and may lose value.

© 2026 PPM America, Inc. All rights reserved.